Have you ever felt like you’ve been running in an all-out sprint only to realize that you haven’t really made any progress at all? Or that you just ran 5 miles on a treadmill but really did not go anywhere? That’s how many investors have felt over the past 18 months. They feel out of breadth with the fast pace of the markets and all the headline news, political banter, and personal changes in their lives. But then they realize that they were just served up a big giant nothing-burger for dinner.

Have you ever felt like you’ve been running in an all-out sprint only to realize that you haven’t really made any progress at all? Or that you just ran 5 miles on a treadmill but really did not go anywhere? That’s how many investors have felt over the past 18 months. They feel out of breadth with the fast pace of the markets and all the headline news, political banter, and personal changes in their lives. But then they realize that they were just served up a big giant nothing-burger for dinner.

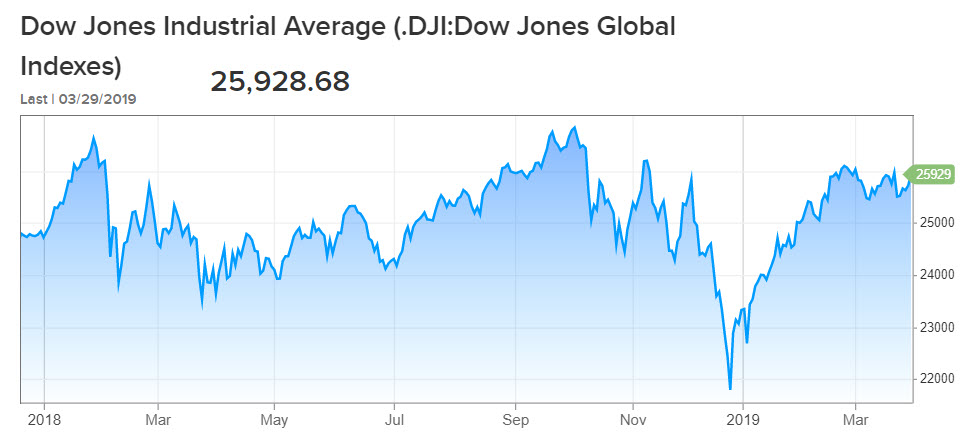

The above chart is the Dow Jones Industrial Index that goes back into the fourth quarter of 2017.

The question is, “As cycles evolve, can you find reasonable valuations in the current marketplace?”

A Look At What Matters – Valuations

I like to remind myself of my long-term principles of investing success. The biggest one is simply, “Buy quality investments at good prices (or even reasonable prices.)” That’s it. Don’t make it any more complicated than it has to be. Can an investor buy quality investments at good prices? If yes, then buy. If no, then build cash and be patient as things move in cycles.

Easier said than done for most people that say they want to build and protect their wealth yet can’t focus on the single most important item that would make that a reality.

“For those wise investors who pay attention to historical norms, we know that 1996 through 2000 was a valuation bubble, and we know that 2003 through 2007 was a debt bubble. Current valuations and debt levels are above those previous examples. What should a rational investor think about today’s situation with a double-whammy in play?”

Just as a friendly public service announcement, the tech bubble led to tech stocks dropping 82% while the S&P 500 dropped over 50%. The global economic meltdown resulted in the S&P 500 dropping 57% over about 18 months while many individual stocks posted losses far greater than that. How do you really think this current bubble is going to end other than painfully just like bubbles of the past?

Just as a friendly public service announcement, the tech bubble led to tech stocks dropping 82% while the S&P 500 dropped over 50%. The global economic meltdown resulted in the S&P 500 dropping 57% over about 18 months while many individual stocks posted losses far greater than that. How do you really think this current bubble is going to end other than painfully just like bubbles of the past?

If you study market history and averages, then it would be important to know that the markets would have to come down about 65% just to get back to long term average valuations. Note that by the very nature of math, markets are both above average and below average for stretches of time to get to “the average.” Thus, it wouldn’t be out of the ordinary for markets to end up “below average” at some point for a stretch of time to reset back to the mathematical average. That’s just something to consider.

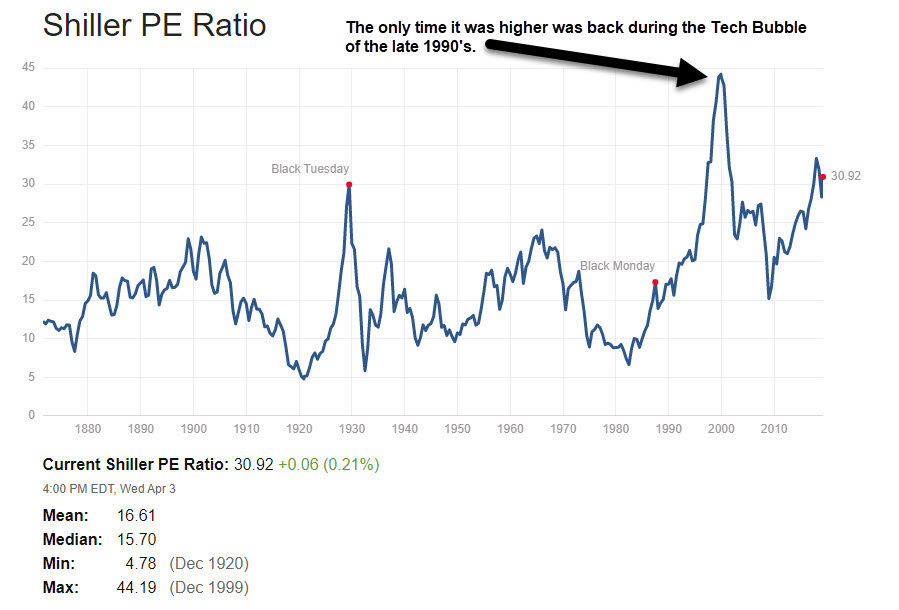

Valuation Metric #1 – Shiller P/E

(also known as CAPE ratio which accounts for the normal impacts of business cycles.) Conclusion – Extreme valuations surpassing those just prior to the Great Depression.

Source: Multpl.com

Source: Multpl.com

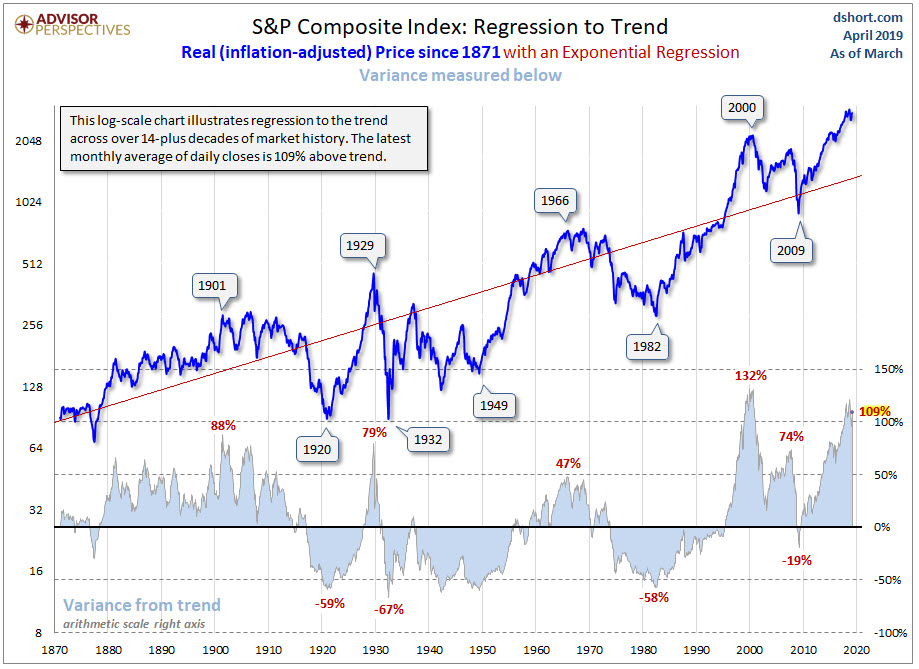

Valuation Metric #2 – S&P Regression To Trend.

The idea here is that things revert back to the mean especially in the stock market and over the long-term, over-performance turns into under-performance and visa-versa. Conclusion – Extreme valuations that have only been higher just before the crash of the tech bubble and significantly higher than levels before the Great Depression and prior to the Global Economic Collapse of 2008-2009.

Source: Advisor Perspectives

Source: Advisor Perspectives

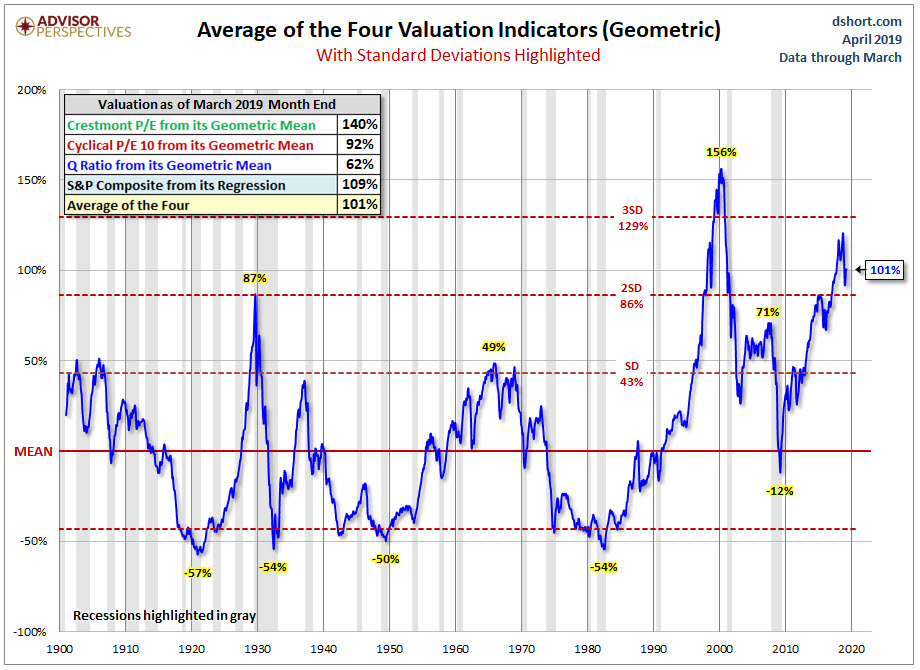

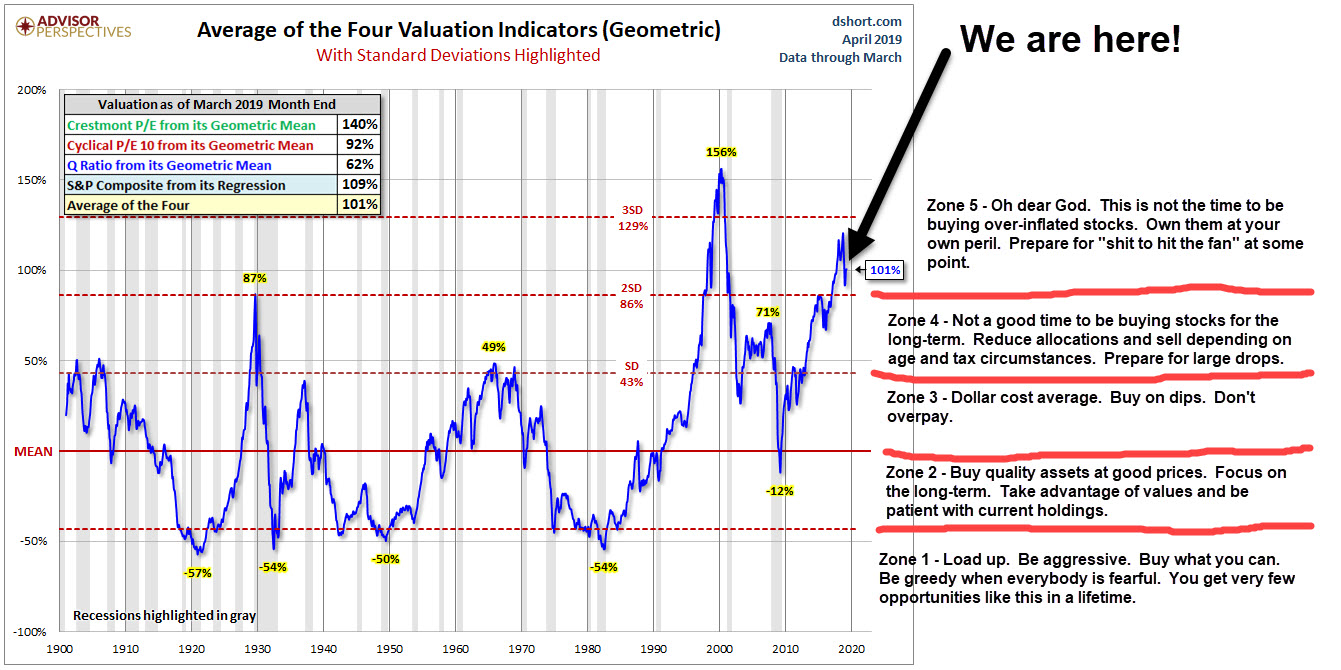

Valuation Metric #3 – Geometric Average of the Four Valuation Indicators.

Using averages of four highly effective but different methods of valuation metrics can provide investors with an overview to ensure that they aren’t just paying attention to one single outlier metric that may not accurately reflect current valuations. Conclusion – Full on bonkers. Buyer beware.

Source: Advisor Perspectives

Source: Advisor Perspectives

Could Extreme Valuations Be Caused By A Mirage Due To Massive Global Stimulus and Interest Rate Policy?

We know a couple of things;

- We know that collectively central bankers around the world have initiated trillions upon trillions of dollars of monetary stimulus since the global crisis ended in 2009. It was what many felt they “had to do” to save the financial system. But then once they saved the system, they just kept on stimulating. Why ruin a good party when people are just starting to feel good?

- We know that central bankers around the world drove interest rates down to levels never seen before.

- We know that sovereign nations, municipalities, corporations and individual households borrowed money at insane levels because, after all, “Hey, the interest rates are so low that it’s like it is free money!”

- Global debt is now appearing to be a runaway train. It’s a $244 trillion global debt bomb (about 3 times the size of the global economy).

But now we are left with a few tiny HUGE problems;

- Our own Federal Reserve told us that they had a good plan to get us out of the old crisis. The plan was to lower interest rates and accumulate a large federal balance sheet (over $4 trillion dollars) and that when the time was right, they would just raise interest rates and reduce the balance sheet and we will all live happily ever after.

- Extreme stock valuations

- Negative interest rates around the world

- Mind blowing levels of debt that are now appearing as though they can never be paid back.

- Global political fracturing.

In 2018, the Federal Reserve told us that they would continue to raise interest rates to normalize them back to reality. They also told us that they would start reducing the balance sheet back to practical levels. But then a little problem occurred…markets started to crash in the fourth quarter of 2018. Major indexes were down 20% very quickly. And then the Fed did something that was very revealing…within three weeks they had a complete change of heart and said that they were no longer going to raise rates and they would stop the balance sheet reduction.

Phewww! For a minute I thought they were serious about having natural, organic, and free markets… At least we can go to bed at night knowing that the manipulation will continue as they have no “Plan B” and no more ammunition when the next recession and crisis hits.

After all, how much lower can we make interest rates around the world if they are already negative in major markets like Germany and Japan? There is currently over $10 Trillion in negative interest debt around the world. Negative interest rates mean that the BORROWER is paid to borrow money. “Here, take my money, I’ll pay you…”

Stock valuations are at extreme levels only surpassed by the tech bubble in the late 1990’s when we had companies with zero revenues and earnings valued at billions of dollars (which led to technically earnings multiples of “infinity.”) The only other time besides the tech bubble where we’ve had stock valuations even close to the current levels is right before the Great Depression. We have long surpassed the valuation levels that preceded the global economic meltdown of 2008-2009.

Many will argue that times were different in 2008-2009 because that was a debt crisis. The only problem is that global debt levels are far higher than those that we had in the early 2000’s.

But it’s not all bad news for stock investors. As value investors we are quite aware that things go in cycles. They always have and they always will. Cycles come and go even if we lose perspective of that somewhere along the way during a cycle. Some cycles are more extreme than others. But we are always somewhere within a greater cycle.

Fundamental investing and long-term success comes down to two proven principles of success;

- Buy quality assets/investments

- Buy at good prices (or even reasonable prices)

That’s the secret sauce of investing. Can an investor buy quality investments at reasonable prices (or better yet bargain prices?)

But investing prudently is much harder to do when you forget that things go in cycles, when the pace is fast, the media is blaring, politicians are trying to get re-elected, your neighbor is driving a new car and bragging about stock market gains, your kid has a soccer game at 5:30pm and you are running late. It’s too easy to follow the masses and BUY, BUY, BUY!!! It must be safe if everybody else is doing it and no problems have presented themselves (YET…)

But that’s exactly how Wall Street loots savers out of their hard-earned money. They tell us that there is never a bad time to buy stocks. They tell us to keep buying, keep holding, because after all, “Aren’t you in it for the long-haul?”

They must get us to believe that as part of their business model. Can you imagine what would happen to Wall Street if they told us to be cautious and tentative? They would miss their quarterly earnings, and annual goals. They would miss their bonuses and stock options. They would lose their customers to another firm that is telling them to BUY, BUY, BUY and creating visions of easy money.

You see, Wall Street has never (AND WILL NEVER) EVER tell people to be cautious. Yet, cycles proceed, markets crash, and people lose money. Then the entire cycle starts all over again. And the cycle will start all over again just like it has in the past. It’s just some individuals and companies (and governments) will be dead on the other side of the cycle. The world will move on without them. They will be buried in the Wall Street Graveyard never to be heard from again or remembered. Because the world moves on without them.

If we could only keep our wits in a crazy world. If we could only follow proven principles of success when it counts the most. If we could only remember – “Buy low and sell high”, rather than, “Buy no matter the extreme price because everybody else is too so it must be ok because Wall Street says so…”

What is a problem for one person will become an opportunity for another. If you know things go in cycles, and you prevent yourself from buying high, that just leaves you in a fantastic position to buy low as the cycles work themselves out.

Tricks To Keep You Safe (and Make You Money As A Long-Term Investor)

What if investing for the long-term could be simplified greatly? What if there were tools to tip you off as to the valuation levels in the equity markets? Wouldn’t that be nice? But here’s the good news…THERE ARE TOOLS! If an investor could follow these valuation signals, they would win over the long-term and avoid major catastrophe’s that wipe out investors and crush their dreams and lives. Are you ready for it?

Let’s take the same Valuation Indicator model provided above and break things out into five investing zones. Keep in mind, that most of the time, equity markets are in zones 2 and 3. Occasionally we find ourselves in zones 1 and 4. It is extremely rare that equity markets find their way into the stratospheres of zone 5. Frankly, we’ve only been in zone 5 once before and that was preceding the tech bubble of the late 1990’s. You know how that ended. The NASDAQ crashed about 80% afterwards and many investors got completely wiped out. But…here we are again.

But Do You Have $112 BILLION Saved Up In Cash?

As the manipulated market continues, I get no shortage of calls from frustrated savers telling me that they have cash that they are anxious to deploy. I hear it all of the time;

- “I have a few thousand dollars saved up. What should I buy?!”

- “I have a few hundred thousand dollars saved up. What should I buy?!”

- “I have a few million dollars saved up. What should I buy?!”

Then I ask them, “But do you have $112 BILLION saved up?” The answer is always, “No. That would be insane and crazy to have that much cash.” Then I tell them that Warren Buffett, perhaps the greatest investor ever, who manages Berkshire Hathaway which has about $112 BILLION dollars stored up that is just sitting on the sidelines.

Warren Buffett is the quintessential value investor. He is the master of buying quality investments at good prices. He’s been doing it for decades. He’s all about buying low. Why is it that the world’s greatest investor could tell us straight to our face,

“Here’s how you make and keep money over the long-term on Wall Street…You buy quality investments at good prices. Don’t overpay. Be fearful when others are greedy and greedy when others are fearful,”

but then hardly anybody follows those guidelines.

Rather, investors can’t stand themselves. They get in their own way. They get caught up in manias and bubbles and euphoria. Most investors get sucked up into sayings like, “But this time is different.” Most investors can’t stay disciplined throughout the entire market cycle. Most investors do the exact opposite of what Warren Buffett preaches. They get caught up in the story of free and easy money and “buy high.” Then when reality sets in and markets exit out of fantasy land, the prices drop and what do they do when prices drop? They sell.

If you are doing a great job of building up cash reserves, pat yourself on the back for a job well done. Keep going. Don’t get sucked into the madness of the crowds and overpay for investments. Remember that things go in cycles. Sometimes investments can be over-valued and sometimes investments can be under-valued. Don’t jumble them up and believe that all points in the cycle are the same. They aren’t. It’s not even close.

Pay attention to stock investors like Warren Buffett. Ask yourself if you are following their proven principles of success. Do you see Warren Buffett changing his principles based upon GDP data or labor reports or who is elected into political office? Do you see Warren Buffett during bubble cycles buying annuities, chasing hotel real estate deals, or investing in hot IPO’s?

What you see Warren Buffett do is follow his basic principles of success. He buys low and if he can’t find good investments at good prices, he accumulates cash (and lots of it). He doesn’t give up on the stock market. He doesn’t buy the S&P 500 index because everybody else is doing it. He doesn’t go and put all his cash into CD’s at Wells Fargo. He stays focused. He remembers that markets move in cycles. He hunts for deals and most of all, he doesn’t break his principles regarding valuations.

We should all be more like Warren Buffett.

Three rules to live by when investing your hard-earned money;

- Buy low and sell high (that’s not the same as buy high and pray because you are under saved and have too much debt from overspending and failure to budget during your lifetime.)

- Don’t lose your money in the stock market.

- Don’t forget that Wall Street is loaded with greedy filthy whores who are only worried about THEIR money, not yours.

Wall Street firms are NOT your friends. The central bankers are NOT your friends. The government is NOT your friend. Big banks that want to load up everyone with debt are NOT your friends. Big corporations are NOT your friends. The mainstream media is certainly NOT your friend.

It’s important to remember that the mainstream media has a customer and it’s not you. Their customers are corporations and Wall Street. The media’s job is to attract eyeballs for advertising. They accomplish this through the creation of stories that revolve around conflict, outrage, and deflection. Even if you are a consumer of business news, the media will do everything to deflect from what is important. They will try and make you think that your future wealth is based upon the labor force participation rate, GDP arithmetic, inflation numbers, the price of oil, fluctuations in interest rates, China industrial output, and where the hot money is. It’s everything except the single most important factors in all of investing which happens to be PRICE and VALUATIONS.

Nothing is more important than the price that you pay for an investment. It’s the golden rule of investing. Simply put, the price you pay has more to do with your future returns than any other factor. Pay too much up front and your future gains will be muted. Take note when you pay attention to the media and what they are serving you. They will spend all their time covering topics except the most important topic of them all, which is the valuation levels of investments. Your long-term investment success depends on your ability to focus on what truly is important and tune out the rest.

So back to your “friends.” None of these institutions care about you personally. They never have and they never will. It’s up to YOU to protect yourself and your capital and use these times in history to position yourself for wealth accumulation over the longer-term time-frame.

When cycles end, prices come down. When prices come down, investors want to jump off the bandwagon and stop losing money. So, they sell. The more that they sell, the more prices come down. The more prices come down, the more people want to sell. That’s why cycles work in both directions. The cycle feeds upon itself.

The winners are the ones that are going against the grain and going in the opposite direction (like Warren Buffett.) They are buying when others are selling (and selling when others are buying). It makes perfect sense even if the masses WON’T DO IT.

Do you want to know why Warren Buffett is one of the richest people on earth? Is it because he does things just like everybody else? Of course not. If he did things like everybody else, he’d be just like everybody else (broke and up to their eyeballs in debt.) But he’s not up to his eyeballs in debt and he’s sitting on a mountain of cash $112 Billion dollars high.

What is your plan? What is your strategy? What are your behaviors?

Are you hoping that the central bankers will be able to stimulate forever until you can buy a Caribbean Island and live happily ever after?

Here’s What Every Investor Should Be Focused On:

- Driving income up and attempting to sustain income in an economy that makes this harder to do with each passing day.

- Living below your means.

- Building up emergency funds.

- Building up cash stockpiles to invest when opportunities arise in the future.

- Paying off your debts. Get rid of those auto payments. Get rid of those house payments. Dump the debt and escape the financial slave masters.

- Investing prudently. Buy low and sell high. Don’t ignore valuations when making investment decisions – EVER!

- Don’t lose your money on bad math bets, even if your neighbor appears to be profiting from that strategy in the short run. Bad math usually ends with horrible results. Remember that most of your neighbors are loaded up to their eyeballs in debt. Their only hope is for a home run or a lottery ticket because they are living way above their means.

Finally, stay healthy. Do you want to know a quick path to wealth reductions and unhappiness? Get sick. The cost of healthcare continues to rise to unaffordable levels. When you get sick, your energy drops, your happiness drops, and you become unproductive. You can’t earn money when you are sick. You don’t have much fun when you are sick. You spend lots of money trying to fix yourselves.

Work on prevention. Don’t wait until you are sick to invest in yourself and your health. Your wealth depends on it (and your happiness does too).

If you should have any questions or need to talk, please feel free to contact me.