You may never have realized it or looked at personal finance this way, but your financial behaviors and habits are linked to your feelings. The good thing about reading a wealth blog is that you can read it and think about it in the privacy of your own little world, without having to openly discuss it with others (especially your financial advisor). In many households, it’s the husband who deals more with the finances of the household and men usually don’t like talking about their feelings.

So many times our feelings about money stem from our childhood. The environment we grew up in often shapes how we handle money as an adult. Bradley Klontz and Ted Klontz are financial psychologists. They use a term called “money scripts” that describes how we feel and our core beliefs about money. “Money scripts are typically unconscious, developed in childhood, passed down from generation to generation within families and cultures, contextually bound, and often only partial truths”.

I find this to be true when reflecting on my childhood. My great-grandmother immigrated to the United States alone at the age of 14. She was from Poland and did not speak English at the time of her journey. When she arrived, she settled in a Polish section of Niagara Falls, NY and began taking on any jobs she could find to survive which was often cleaning houses or helping others. My father was a union electrician and a construction worker. My mother who was a nurse was a stay-at-home mother caring for her six children and the great-grandmother who was now living with us at the time. There were nine of us living in a one-bathroom house on one construction-based inconsistent income. As I entered adulthood, I based many of my feelings about money on my experiences as a child growing up in that particular environment.

“Money Is the Root of All Evil”

So, is it true what we always hear: “Money Is the Root of All Evil”? Does money have control over who we are and our feelings?

First, money itself is neutral. Money is not good or evil. It knows no difference. How “we” as individuals feel, think about, and treat money is the differentiating factor. A person can use money for wonderful contributions to the world. You can use money for life-saving health care, education, saving polar-bears, or creating wonderful lifetime experiences. Or you can use money for addiction, gambling, control over others, or endless consumption of material goods.

A healthy relationship with money can mean freedom and mental liberation. An unhealthy relationship with money can mean constant stress, anxiety, and paranoia. In either case, money is money. Again, the money is neutral. It’s you who has different feelings and emotions on what money represents.

When people come into my office to talk about their finances, I like to talk about goals and objectives. Goals and objectives usually end up along the lines of the following;

- I want to be financially secure

- I want to be debt free

- I want to be independent

- I want to control my time

- I want to work because I want to, not because I have to (or at a place of my choosing on tasks that are of my choosing).

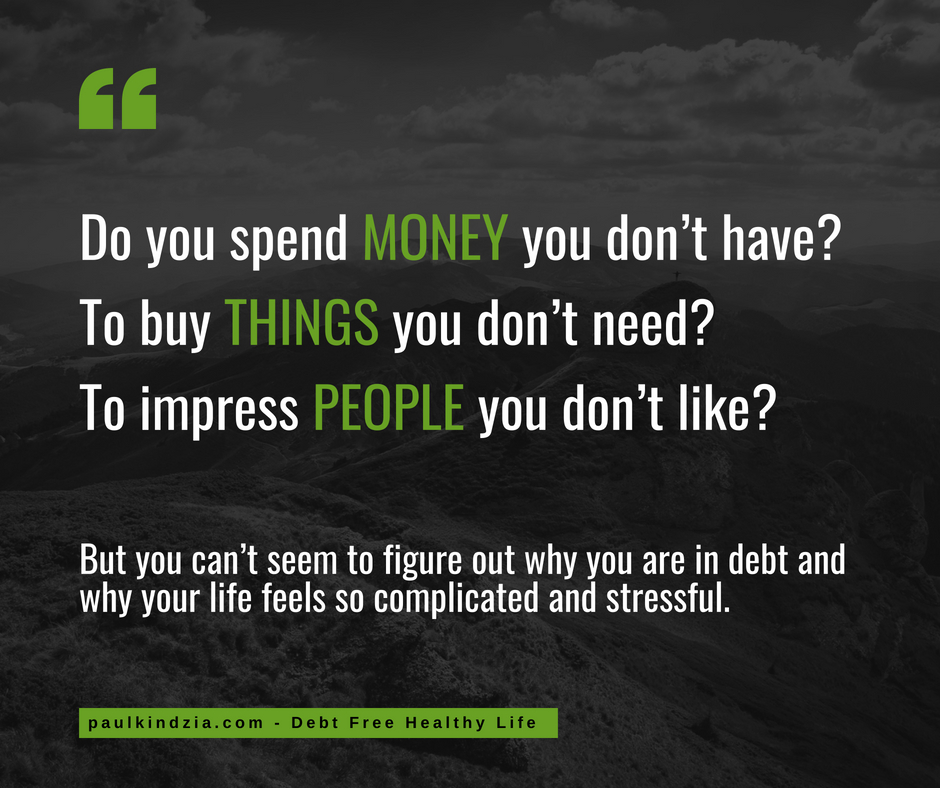

What many don’t realize is that they are chasing what I call “financial feelings.” Here are 3 positive steps to improving your financial feelings;

- Understand and acknowledge that you are chasing “financial feelings” to begin with. What you want is to “feel” financially secure. You want to “feel” independent. You want to “feel” in control of your own destiny or life. There’s not a “one number fits all” to make everybody feel the same way about their own life and situation. One person can have $500,000 to their name and feel very secure while another can have a few million and feel very insecure. Spend time on figuring out what it is you are trying to feel and then determine what it would take to make you feel that way (and why).

- Your spending habits impact your financial feelings. More money can offer you more luxuries and perhaps a better lifestyle. But your spending can also make you “feel” more stressed, anxious and time crunched. As you know, money doesn’t grow on trees so the more you want, the more you have to earn it (which takes a lot of time, effort, and energy). Time spent working means less time doing something else. Stop and ask yourself, “How will purchasing this item or service really make you feel once the novelty wears off?” The funny thing about humans is that their lifestyle expectations tend to keep increasing throughout life. Basically the more you have, the more you want. (And you wonder why you feel like you are always on a treadmill that keeps getting faster and you have no idea how to get off?)

- Prioritize your financial feelings around all purchases (especially large ones like homes and cars). Let me give you an example. Let’s say that you desperately want a new luxury home and are justifying it because the urge is so strong (and of course “you feel” you deserve it right now). Ask yourself some of the following;

- How would living in this mansion or luxury home make you feel?

- How would taking on massive mortgage debt make you feel if that was the only way you could purchase the luxury home?

- How does knowing that you would be on track for a bleak retirement make you feel if you purchased the luxury home?

- How would the stress and anxiety of keeping up with all of the cash flow requirements on the home make you feel?

- How would sacrificing in other areas of your life like vacations, clothes, cars, child expenses, and hobbies make you feel?

- Notice that feelings start to collide. You may feel great about yourself living in a luxury home. You may feel important. You may feel successful. You may feel proud (all good feelings). But are those feelings enough to trump the other feelings that you’ll have if you do the deal? Ideally, you know you are making good decisions when there are little to no negative feelings associated with the purchase of an item or service. On a related note, it’s not uncommon for many successful people to actually “feel guilty” when they purchase something nice because “they feel” that they either don’t deserve it or “they feel” it is an unnecessary purchase. This can happen with people who most easily can afford the luxury item.

- Would you buy the luxury home if no one ever visited you or saw you expensive luxury home? Are you buying the home for you or to impress others?

I know, I know, you don’t want to talk about your feelings. I get it. But I recommend that you take some time to assess your feelings. If you are feeling escalating stress, anxiety and pressure as your net worth or the number of luxury assets that you own is increasing, that may be a tip off that something is amiss and needs some deeper consideration. The goal is to feel more secure and comfortable as we increase wealth. The goal is not to feel more stressed and anxious as we buy more and get more into debt.