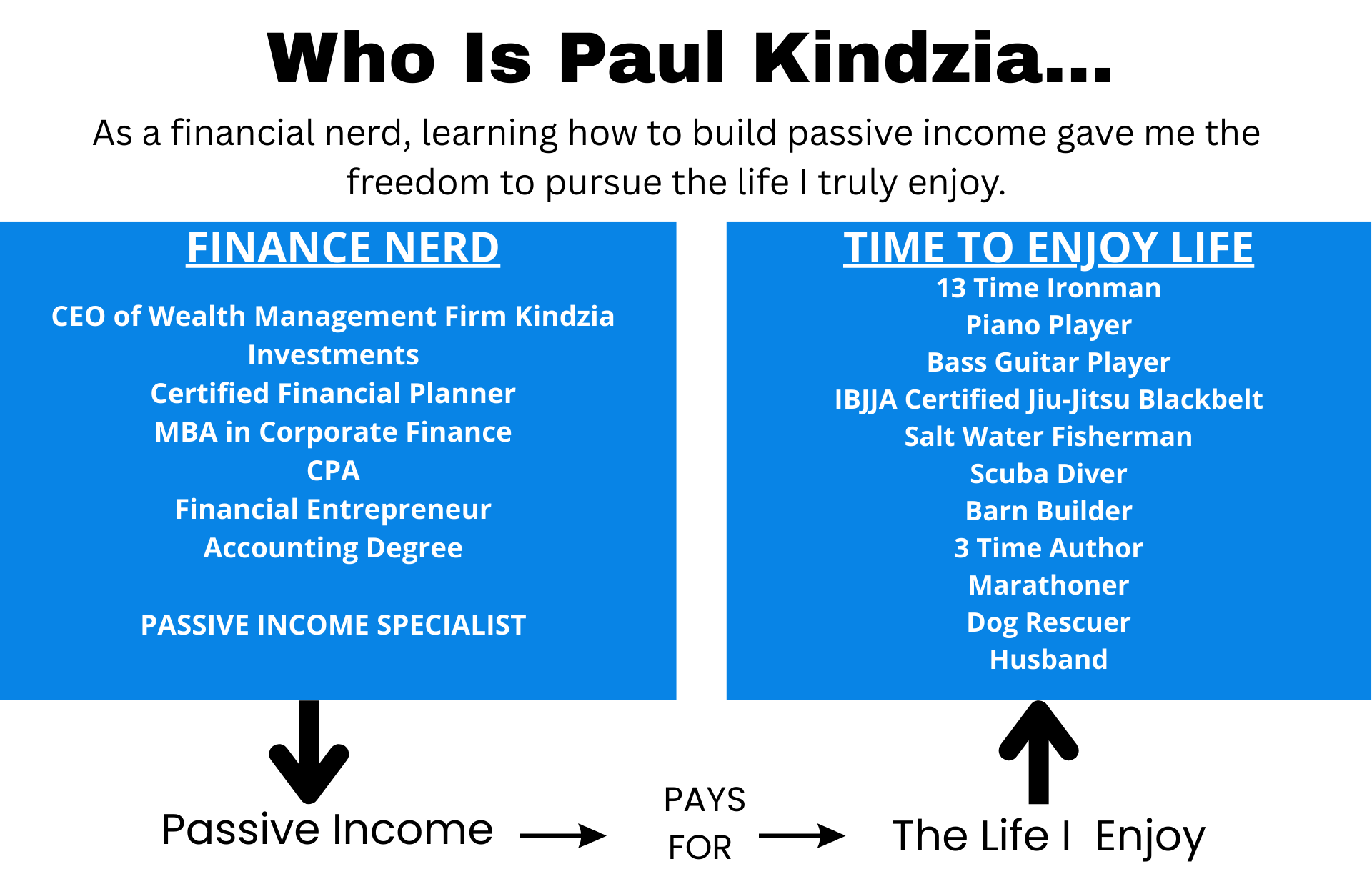

Is your TIME being spent on what truly matters to you?

Let me help you grow your reliable

PASSIVE INCOME

so you have the freedom—

and the funds—

to enjoy life on your terms.

Achieving amazing things in life takes time.

One of the most powerful ways to reclaim it is by creating a lifestyle that lets you work less and live more—giving you the freedom to focus on what truly matters.

Free Time

is expanded by harnessing the power of

Passive Income

CASH FLOW WISDOM

Quick reads.

Straightforward strategies for passive income.

Sign Up Now

WHY PASSIVE INCOME MATTERS

The Time We Trade For Money

For generations, we’ve been conditioned to believe that success means working a steady 9-to-5 job, Monday through Friday, for 40+ years. It's a routine so deeply ingrained in our culture that most people never stop to question it. We chase promotions, put in overtime, and take pride in being busy—believing that more work will eventually buy us the freedom we crave.

But here’s the irony: in the pursuit of more money, we trade away the one thing we can’t get back—our time. We tell ourselves we’ll enjoy life “later,” once we’ve saved enough, once the kids are grown, once we retire. Meanwhile, we miss out on the very things that bring us joy: time with loved ones, travel, creativity, peace of mind. We sacrifice today for a tomorrow that isn’t guaranteed.

The mindset needs to shift. We can still work and be productive—but instead of pouring all our energy into trading time for money, we should be building systems that let money work for us. PASSIVE INCOME—whether through investments, real estate, royalties, or business income that doesn’t rely on our daily labor—is the key to unlocking that freedom. Not to stop working entirely, but to have the choice to work on our terms, and spend the rest of our time doing what truly matters.

Because at the end of the day, the goal shouldn't be to accumulate as much money as possible—it should be to have enough to live a meaningful life. The real wealth is time. And it’s time we started treating it that way.